What is GSTR 9C (GST Audit Form)?

GSTR 9C is an annual audit form for all the taxpayers having the turnover above 2 crores in a particular financial year. Along with the GSTR 9C audit form, the taxpayer will also have to fill up the reconciliation statement along with the certification of an audit.

Under this, the authorities have also introduced the format of GSTR 9C in the notification No. 49/ 2018 – Central tax dated September 13, 2018.

SAG Infotech is here to provide all the relevant details of GSTR 9 and 9C form and step by step procedure to file them along with the screenshots. The GSTR 9C form has a reconciliation statement for reconciling turnover, input tax credits and tax payments. The taxpayers can also view and download the GSTR 9C form in PDF format.

- Who is Required to File GSTR 9C

- Significance of GSTR 9C Audit Form

- GSTR 9C Due Dates Extension & Penalty Norms

- How to File the GSTR 9C Form?

- General Queries on GSTR 9C Form

- GSTR 9C Filing By Gen GST Software

Simplify GSTR 9C Filing by CBIC

Some exemptions has been done in this form listed below:

- Part of turnover adjustments necessary in Table 5B to 5N is now not mandatory and all the adjustment now necessary to be described in Table 5O;

- Table 12B, 12C and 14 (ITC reconciliation) are now not mandatory;

- Few changes done in the Declaration part also.

What is GSTR 9C Annual GST Audit Form?

As per the rules, all the taxpayer will have to file an annual return form with GSTR 9 but now in an addition to the current rule, Section 35 of CGST Act, 2017, all those taxpayers having turnover exceeding 2 crores in a financial year will have to submit audited annual accounts along with a reconciliation statement in GSTR 9C form.

Who is Required to File the GSTR 9C (GST Audit Form)?

All those taxpayers having the turnover above 2 crores in a financial year are required to file GSTR 9C form along with the reconciliation statement and certification of an audit.

Significance of GSTR 9C Audit Form

GSTR-9C is a reconciliation statement which must be certified by a Chartered Accountant or a CMA. Taxpayers whose aggregate turnover in a financial year exceeds Rs 2 Crores need to file GSTR-9C. The GSTR-9C must be digitally signed by the GST Auditor and must report all discrepancies or liabilities in filing any of the GST returns during the financial year. All additional liabilities arising out of the reconciliation exercise and GST audit must be reported and certified by a CS in GSTR-9C. The GSTR-9c is the only yardstick or indicator for GST Authorities to measure the correctness of GST returns filed by taxpayers during a given financial year.

Due Date Extension for Filing GSTR 9C Audit Form Under GST?

Once again, the Indian government has extended the due date of GSTR 9C (Reconciliation Statement) form for both financial year

- Financial Year 2017-18 – 31st December 2019

- Financial Year 2018-19 – 31st March 2020

Note: “Central Board of Indirect Taxes & Customs (CBIC) notified the amendments regarding the simplification of GSTR-9 (Annual Return) and GSTR-9C (Reconciliation Statement) which inter-alia allow the taxpayers to not to provide split of input tax credit availed on inputs, input services and capital goods and to not to provide HSN level information of outputs or inputs, etc. for the financial year 2017-18 and 2018-19.”

GSTR 9C Audit Form Penalty Norms If Miss the Last Date

- As per the penalty provisions of GSTR 9C audit return form, the taxpayer has to pay Rs. 200 per day as a penalty in which Rs. 100 consist of SGST and Rs. 100 for CGST. Also, it is to be noted that the total penalty cannot exceed 0.25% of the total turnover on which the said penalty is being levied.

Updates in GSTR 9C Reconciliation Form By GST Council 31st Meeting

- FORM GSTR-1 & FORM GSTR-3B returns are required to be filed before the filing of FORM GSTR-9 & FORM GSTR-9C

- FORM GSTR-9 & FORM GSTR-9C cannot be used for availing ITC

- FORM GSTR-9C would include verification by the taxpayer who had uploaded reconciliation statement

Where to Download GSTR 9C Offline Utility?

The government has released the file an annual return form with GSTR 9 which can be filed up by the taxpayers and then uploaded to the portal. The offline utility is given in a zip folder which has to be downloaded:

- To download the offline utility for the GSTR 9C first visit the gst.gov.in portal

- Opt on the download tab on the main menu

- Now click on the offline tools in the option and it will redirect to download page

- Click on download option and extract the file

Where to Find GSTR 9C Online Filing Option on Portal?

Also, there is now available GSTR 9C online utility. To start filing the GSTR 9C reconciliation audit report, perform given steps:

- First of all, login with username id & password on www.gst.gov.in

- After that, the dashboard will open, click on the ‘Annual Return’ tab

- Now click on the financial year for the desired period to file the return, click on the FY 2017-18

- An option like ‘Initiate e-filing’ will appear on the screen, click on that

- But as soon as you will select the filing option, you will be asked for filing GSTR 9 form before you can file reconciliation form.

Items Included While Calculating Turnover for GST Audit:

- All taxable supplies, including intra-state and inter-state apart from the ones which attract a reverse charge, will be included.

- Supplies involved between two business verticals

- Goods or supplies that are sent/received by the job worker on principal to principal basis.

- All export/zero-rated supplies

- Supplies made by agent/job work on behalf of the principal

- All exempt supplies

- All taxes apart from the ones covered under GST. For example entertainment tax paid against the sale of tickets

Items Excluded While Calculating Turnover for GST Audit:

- All inward supplies against which tax is paid under reverse charge.

- All kinds of taxes and cess part of Goods and Service Tax like SGST, CGST or IGST, etc.

- Goods that are received back or supplied to a Job Worker

- Activities that are not part of goods or services under schedule III of the CGST Act

How to File the GST Audit Form GSTR 9C – Step by Step:

- The GSTR-9 has two major parts:

- Part-A: Reconciliation Statement

- GSTR 9C Part-B: Certification

GSTR 9C Part-A: Reconciliation Statement Format

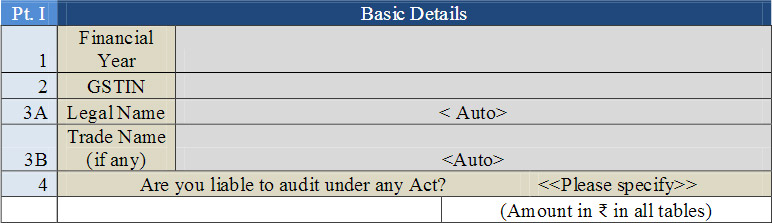

Part 1: Basic Details has the following four sections: Financial Year for which return is being filed.

- 1. Financial Year

- 2. GSTIN of the taxpayer

- 3A. Legal Name of the registered person

- 3B. Trade Name (if any) of the registered business

- 4. If the taxpayer is liable for any audit under this act?

Note: For FY 2017-18, it will contain details for July 2017 to March 2018 period.

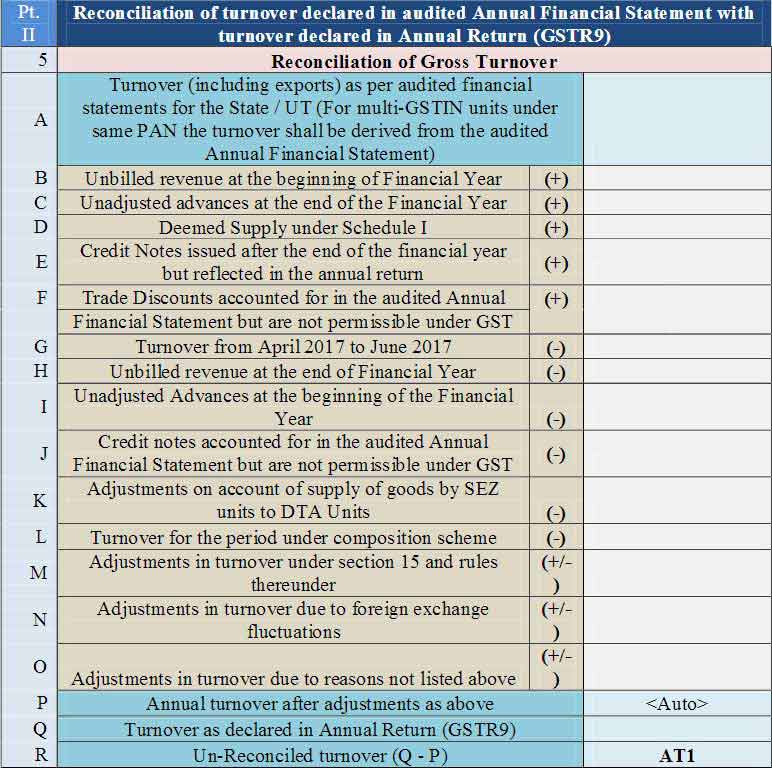

Part 2: Reconciliation of turnover declared in the audited Annual Financial Statement with turnover declared in Annual Return (GSTR9)

- 5. Reconciliation of Gross Turnover

- 5A. Turnover (including exports) as per audited financial statements for the State / UT (For multi-GSTIN units under same PAN the turnover shall be derived from the audited Annual Financial Statement): The turnover as per the audited Annual Financial Statement shall be declared here. There may be cases where multiple GSTINs (State-wise) registrations exist on the same PAN. This is common for persons/entities with a presence over multiple States. Such persons/entities will have to internally derive their GSTIN wise turnover and declare the same here. This shall include export turnover (if any). It may be noted that reference to audited Annual Financial Statement includes reference to books of accounts in case of persons/entities having a presence over multiple States.

- 5B. Unbilled revenue at the beginning of Financial Year (+): Unbilled revenue which was recorded in the books of accounts on the basis of accrual system of accounting in the last financial year and was carried forward to the current financial year shall be declared here. In other words, when GST is payable during the financial year on such revenue (which was recognized earlier), the value of such revenue shall be declared here.

- C. Unadjusted advances at the end of the Financial Year (+): Value of all advances for which GST has been paid but the same has not been recognized as revenue in the audited Annual Financial Statement shall be declared here.

- D. Deemed Supply under Schedule I (+): an Aggregate value of deemed supplies under Schedule I of the CGST Act, 2017 shall be declared here. Any deemed supply which is already part of the turnover in the audited Annual Financial Statement is not required to be included here.

- E. Credit Notes issued after the end of the financial year but reflected in the annual return (+): an Aggregate value of credit notes which were issued after 31st of March for any supply accounted in the current financial year but such credit notes were reflected in the annual return (GSTR-9)shall be declared here.

- F. Trade Discounts accounted for in the audited Annual (+) Financial Statement but are not permissible under GST: Trade discounts which are accounted for in the audited Annual Financial Statement but on which GST was leviable(being not permissible) shall be declared here.

- G. Turnover from April 2017 to June 2017 (-): Turnover included in the audited Annual Financial Statement for April 2017 to June 2017 shall be declared here

- H. Unbilled revenue at the end of Financial Year (-): Unbilled revenue which was recorded in the books of accounts on the basis of accrual system of accounting during the current financial year but GST was not payable on such revenue in the same financial year shall be declared here.

- I. Unadjusted Advances at the beginning of the Financial Year (-): Value of all advances for which GST has not been paid but the same has been recognized as revenue in the audited Annual Financial Statement shall be declared here.

- J. Credit notes accounted for in the audited Annual Financial Statement but is not permissible under GST (-): an Aggregate value of credit notes which have been accounted for in the audited Annual Financial Statement but were not admissible under Section 34 of the CGST Act shall be declared here

- K. Adjustments on account of supply of goods by SEZ units to DTA Units (-): an Aggregate value of all goods supplied by SEZs to DTA units for which the DTA units have filed the bill of entry shall be declared here.Easy Guide to GSTR 9C GST Audit Form with Online Return Filing Process

- L. Turnover for the period under composition scheme (-): There may be cases where registered persons might have opted out of the composition scheme during the current financial year. Their turnover as per the audited Annual Financial Statement would include turnover both as for composition taxpayer as well as the normal taxpayer. Therefore, the turnover for which GST was paid under the composition scheme shall be declared here.

- M. Adjustments in a turnover under section 15 and rules thereunder (+/- ): There may be cases where the taxable value and the invoice value differ due to valuation principles under section 15 of the CGST Act, 2017 and rules thereunder. Therefore, any difference between the turnover reported in the Annual Return (GSTR 9) and turnover reported in the audited Annual Financial Statement due to the difference in valuation of supplies shall be declared here.

- N. Adjustments in turnover due to foreign exchange fluctuations (+/- ): Any difference between the turnover reported in the Annual Return (GSTR9) and turnover reported in the audited Annual Financial Statement due to foreign exchange fluctuations shall be declared here

- O. Adjustments in turnover due to reasons not listed above (+/-): Any difference between the turnover reported in the Annual Return (GSTR9) and turnover reported in the audited Annual Financial Statement due to reasons not listed above shall be declared here.

- P. Annual turnover after adjustments as above

- Q. Turnover as declared in Annual Return (GSTR9): Annual turnover as declared in the Annual Return (GSTR 9) shall be declared here. This turnover may be derived from Sr. No. 5N, 10 and 11 of Annual Return (GSTR 9)

- R. Un-Reconciled turnover (Q – P) AT1

- 6. Reasons for Un – Reconciled difference in Annual Gross Turnover

- Reasons for non-reconciliation between the annual turnover declared in the audited Annual Financial Statement and turnover as declared in the Annual Return (GSTR 9) shall be specified here.

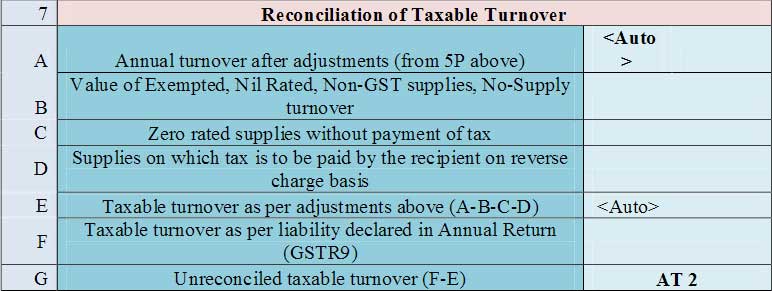

- 7. Reconciliation of Taxable Turnover

- The table provides for the reconciliation of taxable turnover from the audited annual turnover after adjustments with the taxable turnover declared in annual return (GSTR-9).

- A. Annual turnover after adjustments (from 5P above): Annual turnover as derived in Table 5P above would be auto-populated here.

- B. Value of Exempted, Nil Rated, Non-GST supplies, No-Supply turnover: Value of exempted, nil rated, non-GST and no-supply turnover shall be declared here. This shall be reported net of credit notes, debit notes and amendments if any.

- C. Zero-rated supplies without payment of tax: Value of zero-rated supplies (including supplies to SEZs) on which tax is not paid shall be declared here. This shall be reported net of credit notes, debit notes and amendments if any.

- D. Supplies on which tax is to be paid by the recipient on reverse charge basis: Value of reverse charge supplies on which tax is to be paid by the recipient shall be declared here. This shall be reported net of credit notes, debit notes and amendments if any

- E. Taxable turnover as per adjustments above (A-B-C-D): The taxable turnover is derived as the difference between the annual turnover after adjustments declared in Table 7A above and the sum of all supplies (exempted, non-GST, reverse charge etc.) declared in Table 7B, 7C and 7D above.

- F. Taxable turnover as per liability declared in Annual Return (GSTR9): Taxable turnover as declared in Table 4N of the Annual Return (GSTR9) shall be declared here.

- G. Unreconciled taxable turnover (F-E)

- 8. Reasons for Un – Reconciled difference in taxable turnover

- Reasons for non-reconciliation between adjusted annual taxable turnover as derived from Table 7E above and the taxable turnover declared in Table 7F shall be specified here.

Part 3: Reconciliation of tax paid

- 9. Reconciliation of rate wise liability and amount payable thereon

- The table provides for the reconciliation of tax paid as per reconciliation statement and amount of tax paid as declared in Annual Return (GSTR 9). Under the head labelled ―RC‖, supplies where the tax was paid on reverse charge basis by the recipient (i.e. the person for whom reconciliation statement has been prepared ) shall be declared with GSTR 9 file an annual return form with GSTR 9

- P. Total amount to be paid as per tables above: The total amount to be paid as per liability declared in Table 9A to 9O is auto-populated here

- Q. The total amount paid as declared in Annual Return (GSTR 9): The amount payable as declared in Table 9 of the Annual Return (GSTR9) shall be declared here. It should also contain any differential tax paid on Table 10 or 11 of the Annual Return (GSTR9)

- 10. Reasons for un-reconciled payment of amount: Reasons for non-reconciliation between payable / liability declared in Table 9P above and the amount payable in Table 9Q shall be specified Part-B: Certification.

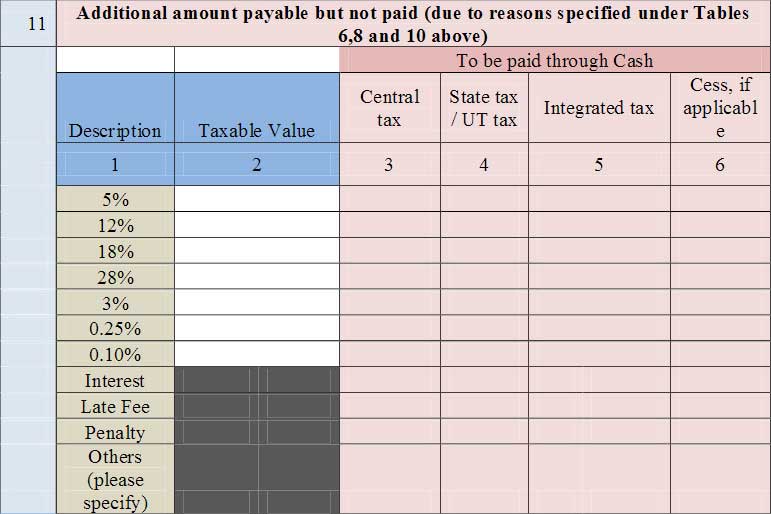

- 11. Additional amount payable but not paid (due to reasons specified under Tables 6,8 and 10 above): Any amount which is payable due to reasons specified under Table 6, 8 and 10 above shall be declared here.

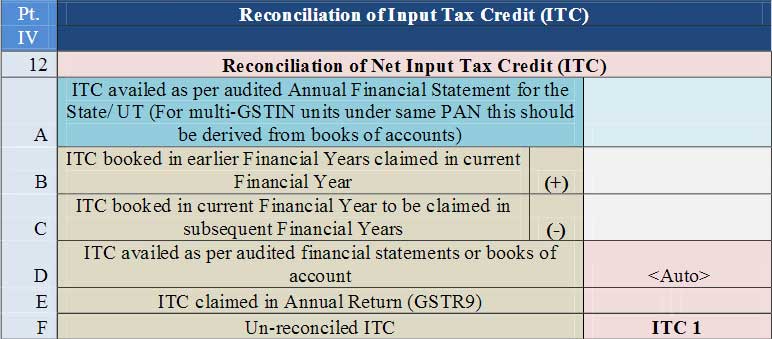

Part 4: Reconciliation of ITC (Input Tax Credit)

- 12. Reconciliation of Net ITC (Input Tax Credit)

- A. ITC availed as per audited Annual Financial Statement for the State/ UT (For multi-GSTIN units under same PAN this should be derived from books of accounts): ITC availed (after reversals) as per the audited Annual Financial Statement shall be declared here. There may be cases where multiple GSTINs (Statewise) registrations exist on the same PAN. This is common for persons/entities with a presence over multiple States. Such persons/entities will have to internally derive their ITC for each individual GSTIN and declare the same here. It may be noted that reference to audited Annual Financial Statement includes the reference to books of accounts in case of persons/entities having the presence over multiple States.

- B. ITC booked in earlier Financial Years claimed in current Financial Year (+): Any ITC which was booked in the audited Annual Financial Statement of an earlier financial year(s)but availed in the ITC ledger in the financial year for which the reconciliation statement is being filed for shall be declared here. This shall include transitional credit which was booked in earlier years but availed during Financial Year 2017-18.

- C. ITC booked in current Financial Year to be claimed in subsequent Financial Years (-): Any ITC which has been booked in the audited Annual Financial Statement of the current financial year but the same has not been credited to the ITC ledger for the said financial year shall be declared here.

- D. ITC availed as per audited financial statements or books of account: ITC availed as per audited Annual Financial Statement or books of accounts as derived from values declared in Table 12A, 12B and 12C above will be auto-populated here.

- E. ITC claimed in Annual Return (GSTR 9): Net ITC available for utilization as declared in Table 7J of Annual Return (GSTR9) shall be declared here.

- 13. Reasons for un-reconciled difference in ITC

- Reasons for non-reconciliation of ITC as per audited Annual Financial Statement or books of account (Table 12D) and the net ITC (Table12E) availed in the Annual Return (GSTR9) shall be specified here.

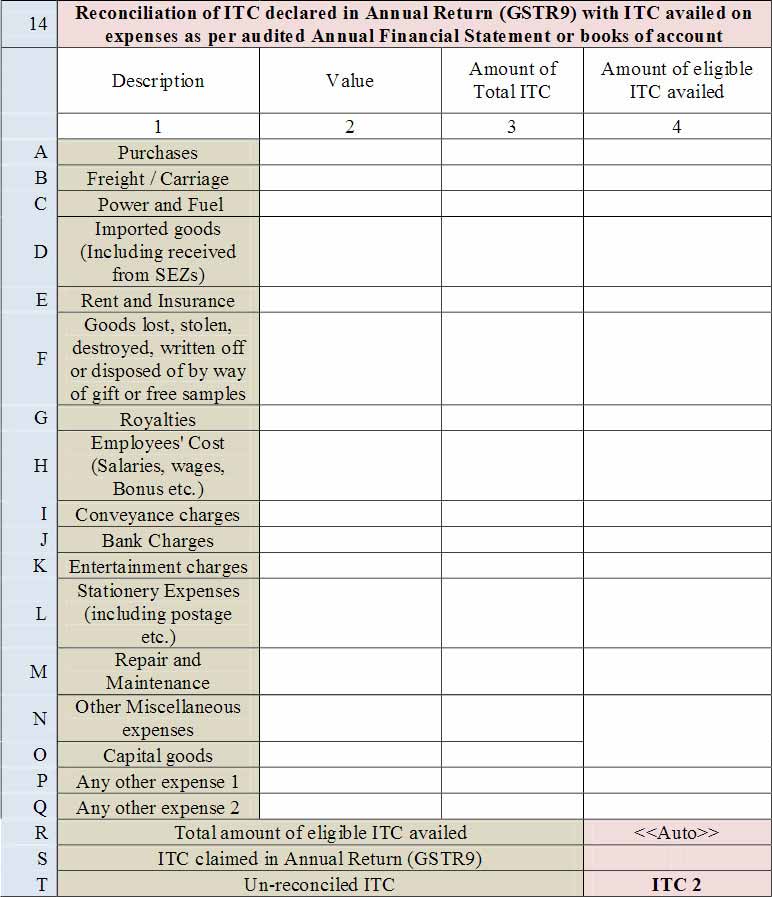

- 14. Reconciliation of ITC declared in Annual Return (GSTR9) with ITC availed on expenses as per audited Annual Financial Statement or books of account.

- This table is for the reconciliation of ITC declared in the Annual Return (GSTR9) against the expenses booked in the audited Annual Financial Statement or books of account. The various sub-heads specified under this table are general expenses in the audited Annual Financial Statement or books of account on which ITC may or may not be available. Further, this is only an indicative list of heads under which expenses are generally booked. Taxpayers may add or delete any of these heads but all heads of expenses on which GST has been paid/was payable are to be declared here.

- A. Purchases

- B. Freight / Carriage

- C. Power and Fuel

- D. Imported goods (Including received from SEZs)

- E. Rent and Insurance F Goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples

- G. Royalties

- H. Employees’ Cost (Salaries, wages, Bonus etc.)

- I. Conveyance charges

- J. Bank Charges

- K. Entertainment charges

- L. Stationery Expenses (including postage etc.)

- M. Repair and Maintenance

- N. Other Miscellaneous expenses

- O. Capital goods

- P. Any other expense 1

- Q. Any other expense 2

- R. Total amount of eligible ITC availed: Total ITC declared in Table 14A to 14Q above shall be auto-populated here.

- S. ITC claimed in Annual Return (GSTR9): Net ITC availed as declared in the Annual Return (GSTR9) shall be declared here. Table 7J of the Annual Return (GSTR9) may be used for filing this Table.

- T. Un-reconciled ITC | ITC 2

- 15. Reasons for the un-reconciled the difference in ITC: Reasons for non-reconciliation between ITC availed on the various expenses declared in Table 14R and ITC declared in Table 14S shall be specified here.

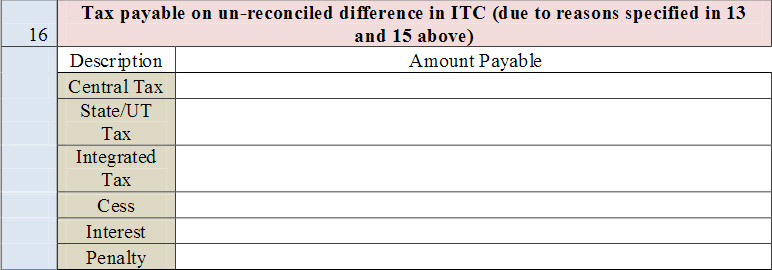

- 16. Tax payable on the un-reconciled difference in ITC (due to reasons specified in 13 and 15 above): Any amount which is payable due to reasons specified in Table 13 and 15 above shall be declared here.

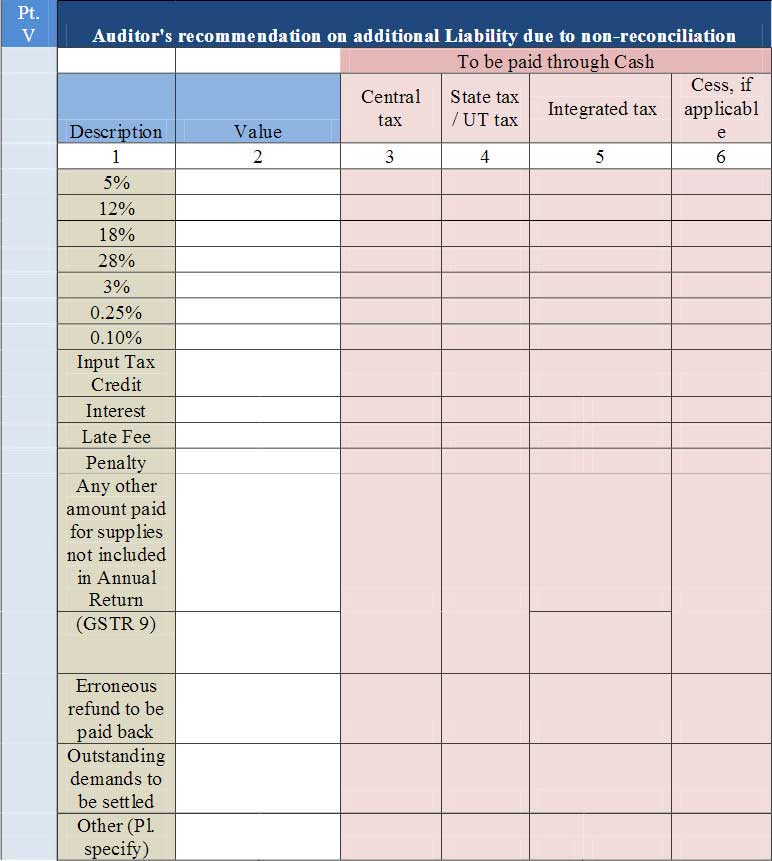

Part 5: Auditor’s recommendation on additional Liability due to non-reconciliation

- Part V consists of the auditor’s recommendation on the additional liability to be discharged by the taxpayer due to non-reconciliation of turnover or non-reconciliation of the input tax credit. The auditor shall also recommend if there is any other amount to be paid for supplies not included in the Annual Return. Any refund which has been erroneously taken and shall be paid back to the Government shall also be declared in this table. Lastly, any other outstanding demands which are recommended to be settled by the auditor shall be declared in this Table.

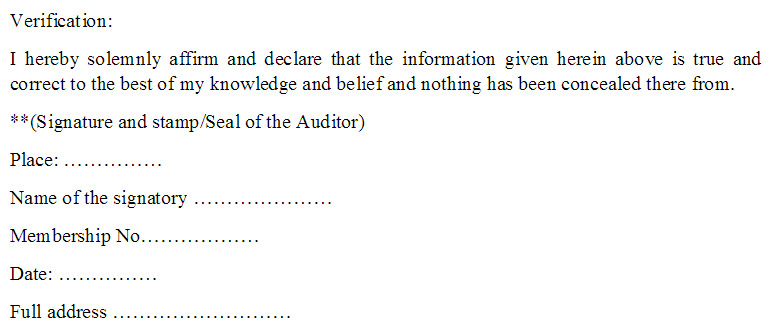

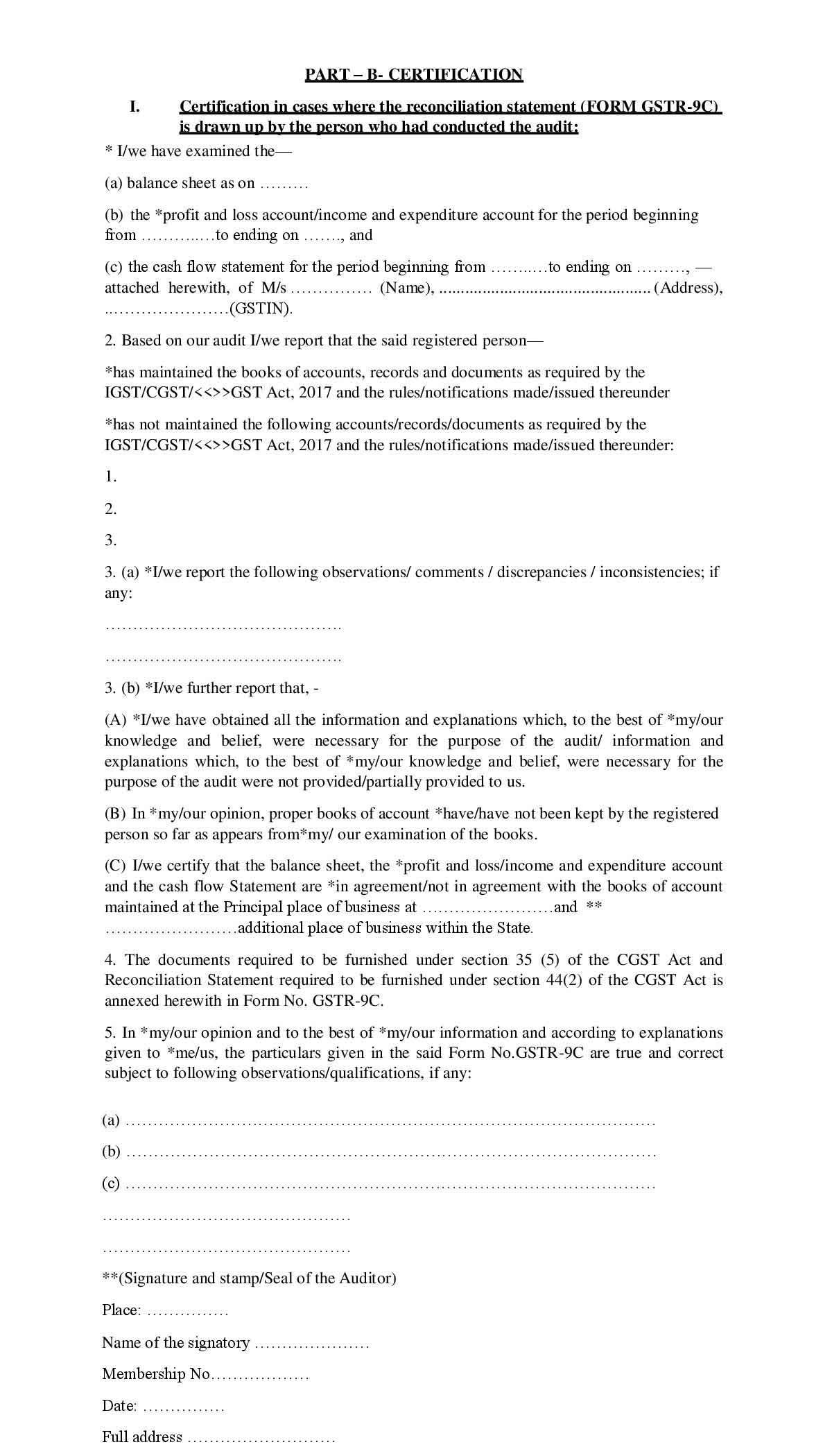

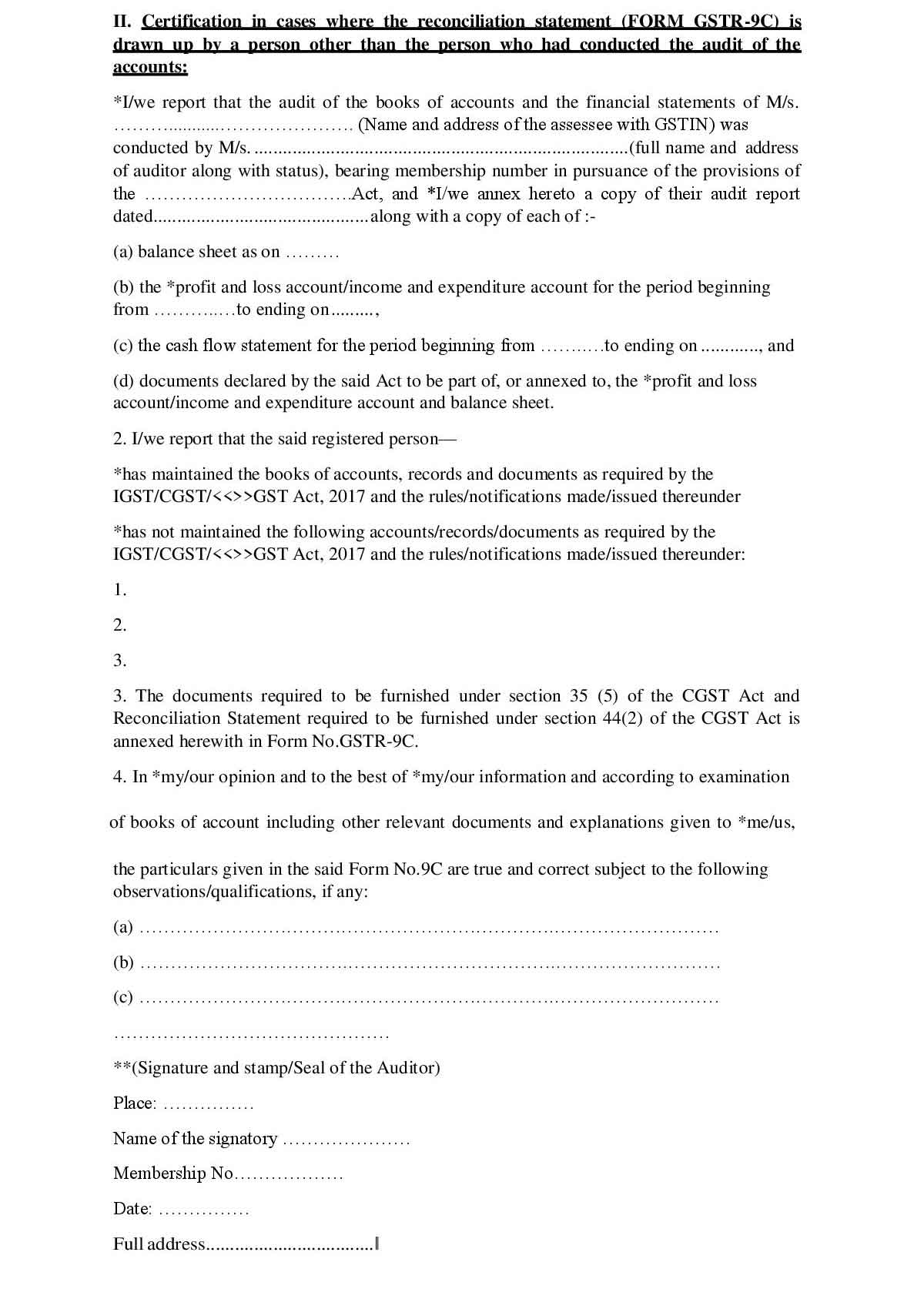

GSTR 9C Part-B: Certification

A certification part is also done once after the GSTR 9 audit is conducted by the person responsible for the audit. The form has two major parts including

1 – Certification in cases where the reconciliation statement (Form GSTR 9C) is drawn up by the person who had conducted the audit.

- A – Balance sheet date

- B – P&L Account including dates

- C – Cash flow statement including dates

2 – Based on audit the auditor mentioned:

Proper maintenance of books status

Or not maintained

Or not maintained

3(A) – Based on any observations done by the auditor, reporting any differences:

3(B) – Further reporting

4 – Documents required under section 35(5) of CGST and reconciliation statement required which are to furnished under section 44(2) of CGST Act annexed in form no. GSTR 9C

5 – All the details and transactional information stated in GSTR form 9C are validated in this point.

Credentials With Signature, Name of the signatory, Membership no. and Date

General Queries on GSTR 9C Form

Q.1 Is the Audit of Accounts maintained by the registered taxable person required to be got done by a Chartered Accountant/Cost Accountant under GST?

As per the GST law, it is mandatory for all the Registered person to get their accounts audited by a chartered accountant or a cost accountant whose aggregate turnover during a financial year exceeds the threshold limit of Rs. 2 Crore. Whence, no such audit is required to be got done by the Chartered or Cost accountant in cases other than mentioned above.

Q.2 – Does ‘aggregate turnover’ deals with topics such as stock transfers/ cross charges effected between branches located in two different states?

Aggregate Turnover has been defined in Section 2(6) of CGST/ SGST Act and the definition of aggregate turnover includes ‘inter-state supplies of a person having the same PAN’. Thus, we see that stock transfers/ cross-charges of services provided from a branch, located in one state to a branch located in another state is included in the definition of Aggregate turnover of the related branch supplying goods/ services.

Q.3 – Does the term ‘aggregate turnover,’ includes stock transfers which are effective within the States having same GSTIN for determining the threshold limits?

The term ‘aggregate turnover’ is not supposed to be included in stock transfers effective within the same state having single GSTIN for the purpose of determining the threshold limit. However, in cases where more than one GSTIN has been allotted for the different branches located in the same state, such branch transfers shall be included for computing threshold limit of Rs. 2 crore to get to the conclusion that whether there is any requirement for audit or not.

Q.4 – Will a Registered Taxpayer who has exclusively exempted supply of goods or services exceeding Rs. 2 crores, would require to fill the GSTR 9C form?

As ‘aggregate turnover’ has been defined under the GST Act, it includes ‘exempt supplies’. Thus, even in the case of a registered person under GST who provides exempted supplies, will have to file Form GSTR 9C.

Q.5 Does the Form GSTR 9C be required to be filed by a person against each registration obtained by him in respect of each of the States?

Provision is that Section 35(5) of SGST Act requires Audit to be conducted in addition to Section 35(5) of CGST Act. Thus, to maintain Compliance audit is required to be conducted state wise as per Section 35(5) of SGST Act. Thus, if we consider an example like if a person is having registration in Karnataka and Tamil Nadu, then he is required to be audited for his accounts under KGST Act, 17 and TNGST Act, 17. The GSTR 9C form is required to be filed under Rule 80(3) of KGST Rules, 2017 and the TNGST Rules. Thus, it is evident that a person registered in more than one state is supposed to file form GSTR 9C registration wise for each and every state.

Q.6 – Is it required for a Chartered Accountant to be got registered as a GST practitioner to get certified the Form GSTR 9C?

A GST practitioner gets authorization for the practice of the below-mentioned rules as per Section 48 of the CGST/ SGST Act under Rule 83(8) of the CGST/ SGST Act:

- a) furnishing the details of outward and inward supplies

- b) to furnish monthly, quarterly, annual or final return

- c) Can make deposits to get amount credited into the electronic cash ledger

- d) he could file a claim for any sort of refund

- e) filing application for getting the registration amended or getting the registration canceled

The GST Act/ Rules does not give the ‘Power to Audit’ to a GST practitioner as per section 35(5). ‘Power to Audit’ is only granted to Chartered Accountants or Cost Accountants. Thus, it is not required for a Chartered Accountant to get registered as a GST practitioner for certifying Form GSTR 9C.

Q.7 – What are the documents to be enclosed along with GSTR 9C?

- Under section 35(5), it is stated that a copy of audited accounts and other such documents in the prescribed manner along with the reconciliation statement (Form GSTR 9C) to be submitted.

- The ‘Prescription’ which is mentioned in the Act should be provided as mentioned in the term ‘as may be prescribed’. Only the audited annual accounts have been prescribed in Rule 80(3) in the name of documents.

- Talking about Part B of GSTR 9C, it is required by the GST Auditor to get a copy of audit report of the entity enclosed where the audit of the entity has been conducted by another person under a statute other than the GST Act.

- In the mentioned case, the documents which has been declared by the statute, which would further be considered as audited financial statements, must be annexed to the audit report.

Q.8 – Should the Form GSTR 9 and Form GSTR 9C get filed separately?

As per Section 44(2) of the CGST/ SGST Act 2017, a Registered person is required to file his Annual return in Form GSTR 9 along with this he has to provide a reconciliation statement through Form GSTR 9C. Thus we see, Form GSTR 9C is required to be filed along with Form GSTR 9 where the turnover exceeds Rs. 2 crores.

Q.9 – Is there any time limit to file Form GSTR 9C?

The Section 44(2) states that the reconciliation statement is required to be provided in Form GSTR 9C along with the Form GSTR 9. Section 44(1), on the other hand, declares the due dates. As per this section, the due date for filing the annual return is on or before the thirty-first day of December following the end of the FY for which the Annual return is prepared. Thus, the conclusion could be drawn that the due date for filing reconciliation statement in Form GSTR 9C is on or before the thirty-first day of December following the end of the financial year for which the reconciliation statement is being prepared.

Q.10 – Could the late fee be waived off in Genuine and special cases?

The Government has the right to get a part or full of the late fee, mentioned in section 47, waived through notification, for such section of taxpayers and under such mitigating and specified circumstances. All this could be done on the recommendation of the Council. However, no such notification is evident to till date issued by the Central Government/ State Government.

Q.11 – Is Audit, mentioned under Section 35(5), be applicable to the Non-Filers or unregistered Persons who are liable to get registered?

- As per Section 35(5) of the CGST Act, only a Registered person is required to get his accounts audited by a CA or CWA. Again, a non-filer is a Registered Person according to Section 25 of the CGST Act, thus he must get audit conducted under Section 35(5) of the said Act. Considering practically, such a person would never had filed his returns and hence, Form 9 & 9C wouldn’t be possible in his case and no audit for him is required.

- Understanding clearly, an unregistered person who is eligible for registration under Section 25 of the CGST is a taxable person. Here, the unregistered Person is not a Registered Person as per Section 2(94) of the CGST Act 2017. Hence, following Section 35(5) of the Act, audit is not required.

Q.12 – Mention the records which are required to be reconciled in Form GSTR-9C?

The records to be reconciled in GSTR-9C are:

- Books of accounts of the registered person – If a registered person has multiple registrations, The required information could be derived from the Audited financials of the entity.

- Annual Return of Registered Person in Form GSTR 9.

Q.13 – What are the contents of Form GSTR 9C?

Form GSTR 9C consists of 2 parts. Part-A consists of Reconciliation statement and Part B is Certificate to be issued by GST Auditor.

Q.14 – What are the details which are to be provided in SI. No.5B (Unbilled revenue at the beginning of Financial Year)?

The unbilled revenue at the beginning of Financial Year are required to be added in Clause 5B. The unbilled revenue recorded on the basis of the accrual system of Accounts in the Books of accounts for the earlier financial year for which the invoice is issued under GST law, is required to be declared here. Understanding more clearly, the value of such Revenue which has been recognized as income during a financial year on which GST is liable to be paid, is required to be mentioned in SI. No.5B

Q.15 – Mention the adjustments to be included/excluded from SI. No.5C of Form GSTR-9C?

The advances which are received could be of various purposes. Therefore, the Advances on which GST is liable should only be considered for the adjustment. The illustrations of advances to be included/excluded are as follows:

Include for Adjustment

| 1. | Advance received in respect of services for which the supply has not been made as on 31st March 2018 | Revenue not recognized in books, but offered to tax for GST |

| 2. | Advance received for Goods before 15th Nov 2017 and the supply of goods not complete as on 31st March 2018 | Revenue not recognized in books, but offered to tax for GST |

Do NOT include for Adjustment

| Sl. No. | Particular’s | Reason |

| 1. | Advance received for EXEMPTED services as on 31St March 2018 | GST is not applicable |

| 2. | Advance received for Goods after 15th Nov 2017 | GST is not applicable |

| 3. | Financial Advances received which are not adjustable against any services | NOT a GST Transaction |

No comments:

Post a Comment